🕵️♀️ [On-chain Sleuth] Topic: CRV Whale & Collaterals 💤

The main topic in the world of DeFi in recent days is a story about the liquidity of the CRV token.

PS: many are fans of Michael as he has been 24/7 in community chats since the early NuCypher days in 2017. Chill, open, and communicative. So this post isn't to beat him into the ground (which isn't even possible) but to discuss the latest things related to CRV collateral. We do like M.C.

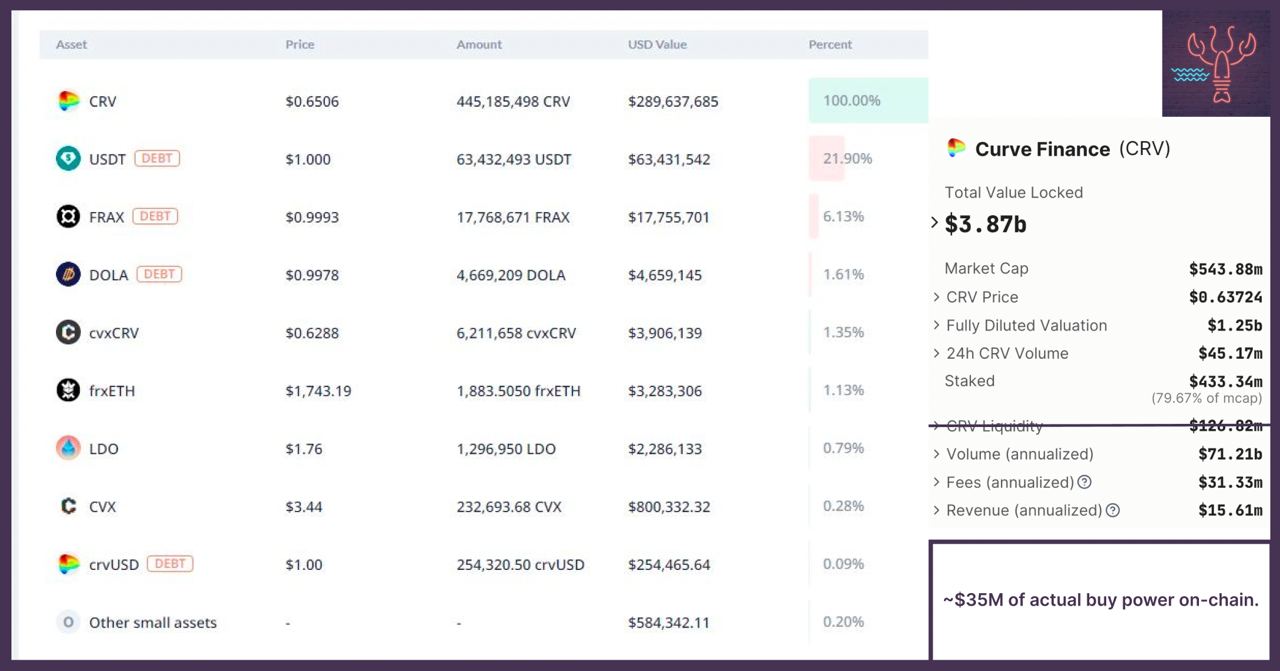

0x7a16ff is the source of a significant $188M collateral provided on Aave - all in CRV (!) with an open position involving a $64.2 million USDT borrowing. The current liquidity on all DEXes combined (that disregards off-chain demand, options, and any other not currently bidding on-chain seen amounts) - is not as big, regardless of what DeFiLlama shows: because half of that is cvxCRV and a half of another half is CRV itself (that's how liquidity numbers are counted in DeFi, a 2x). So the real current liquidity on DEXes is about $35M total buy power.

So is the ratio quite alarming, or do people say so?

Gauntlet (known as math brains) is advising Aave DAO to limit the usage of CRV as collateral. Because what happens is the following: CRV goes down -> 0x7a16ff can add more CRV to support HF (health factor) of their position -> etc... but liquidity is finite! As anywhere, unless your name end with “Powell”. A simple solution is to simply disallow new loans based off CRV. Not to punish, but reduce the dominance.

🤔 At the same time, other DAO members of Aave seem to be appalled by this attack on the community member that has violated nothing and just keeps using math as intended: "You have no idea whether he intends to repay the loan. He may be ecstatic to lose 45% of his collateral’s value, as you noted. But on the other hand, he may believe CRV is massively undervalued, and hence would rather borrow against his CRV holdings than sell at these ridiculously low prices. We just don’t know.”

At present, HF for this open position is 1.68 = ok. However, if this rate experiences a decline and falls below the critical threshold of 1.00, an automatic liquidation of the collateral will occur. The current liquidation price of the position is $0.374, and $CRV is trading at $0.64 now. Ok? Idk. “AT LEAST KNOWN 24% of all CRVs are on the founder’s wallets, with one of the most locked tokens today (and only 15% free float available to sell). At current AMM liquidity, you literally cannot get the price down low enough.” - says threadman Adam.

Again though, this post isn't to find someone guilty or blame - the fact is, oracles & collaterals are HARD. Mostly because of how often things change, like liquidity and CMC/FDV. In many cases, you don't even know who the largest LPs are for a token - and if they are connected at all.

To understand the bigger picture CRV stats at the time of publication:

👻 Aave: $188M CRV collateral -> $63M debt in stables

🧙 Abracadabra: $50M CRV collateral -> $20M debt in stables

⚫️ Fraxlend: $35M CRV collateral -> $16M debt in stables

↔️ Inverse: $7M CRV collateral -> $3M debt in stables

Not nothing, right? The worries aren't totally unbased, because $$ went elsewhere.

💡 Don't shit yourself, loser, watch your own NW!

Well, this stuff is actually pretty relevant to DeFi as a whole. Here is why:

1) Due to potential liquidations, CRV might not have enough liquidity as a token -> bad debt to Aave & other lending protocols

2) CRV going down will mean rewards of many stables will massively drop, causing LPs to exit

3) Due to redemptions mechanisms being based off the (low) market liquidity in many cases, shit can spiral

4) That could cause some stables to temporarily depeg, influencing other collateral positions in DeFi

This is not fractional reserve in any way like FTT, no need to compare to that. However, liquidity crunches are a thing. Unintended shit can happen during the turmoils. Stay safu out there, crabs 🦀

{kind=link}

The main topic in the world of DeFi in recent days is a story about the liquidity of the CRV token.

PS: many are fans of Michael as he has been 24/7 in community chats since the early NuCypher days in 2017. Chill, open, and communicative. So this post isn't to beat him into the ground (which isn't even possible) but to discuss the latest things related to CRV collateral. We do like M.C.

0x7a16ff is the source of a significant $188M collateral provided on Aave - all in CRV (!) with an open position involving a $64.2 million USDT borrowing. The current liquidity on all DEXes combined (that disregards off-chain demand, options, and any other not currently bidding on-chain seen amounts) - is not as big, regardless of what DeFiLlama shows: because half of that is cvxCRV and a half of another half is CRV itself (that's how liquidity numbers are counted in DeFi, a 2x). So the real current liquidity on DEXes is about $35M total buy power.

So is the ratio quite alarming, or do people say so?

Gauntlet (known as math brains) is advising Aave DAO to limit the usage of CRV as collateral. Because what happens is the following: CRV goes down -> 0x7a16ff can add more CRV to support HF (health factor) of their position -> etc... but liquidity is finite! As anywhere, unless your name end with “Powell”. A simple solution is to simply disallow new loans based off CRV. Not to punish, but reduce the dominance.

🤔 At the same time, other DAO members of Aave seem to be appalled by this attack on the community member that has violated nothing and just keeps using math as intended: "You have no idea whether he intends to repay the loan. He may be ecstatic to lose 45% of his collateral’s value, as you noted. But on the other hand, he may believe CRV is massively undervalued, and hence would rather borrow against his CRV holdings than sell at these ridiculously low prices. We just don’t know.”

At present, HF for this open position is 1.68 = ok. However, if this rate experiences a decline and falls below the critical threshold of 1.00, an automatic liquidation of the collateral will occur. The current liquidation price of the position is $0.374, and $CRV is trading at $0.64 now. Ok? Idk. “AT LEAST KNOWN 24% of all CRVs are on the founder’s wallets, with one of the most locked tokens today (and only 15% free float available to sell). At current AMM liquidity, you literally cannot get the price down low enough.” - says threadman Adam.

Again though, this post isn't to find someone guilty or blame - the fact is, oracles & collaterals are HARD. Mostly because of how often things change, like liquidity and CMC/FDV. In many cases, you don't even know who the largest LPs are for a token - and if they are connected at all.

To understand the bigger picture CRV stats at the time of publication:

👻 Aave: $188M CRV collateral -> $63M debt in stables

🧙 Abracadabra: $50M CRV collateral -> $20M debt in stables

⚫️ Fraxlend: $35M CRV collateral -> $16M debt in stables

↔️ Inverse: $7M CRV collateral -> $3M debt in stables

Not nothing, right? The worries aren't totally unbased, because $$ went elsewhere.

💡 Don't shit yourself, loser, watch your own NW!

Well, this stuff is actually pretty relevant to DeFi as a whole. Here is why:

1) Due to potential liquidations, CRV might not have enough liquidity as a token -> bad debt to Aave & other lending protocols

2) CRV going down will mean rewards of many stables will massively drop, causing LPs to exit

3) Due to redemptions mechanisms being based off the (low) market liquidity in many cases, shit can spiral

4) That could cause some stables to temporarily depeg, influencing other collateral positions in DeFi

This is not fractional reserve in any way like FTT, no need to compare to that. However, liquidity crunches are a thing. Unintended shit can happen during the turmoils. Stay safu out there, crabs 🦀